Economics

Context: Policymakers trying to transition India to a less-cash economy have been confounded by a peculiar phenomenon of currency in circulation growing right alongside rising digital adoption.

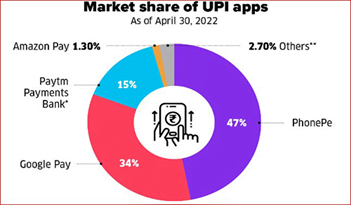

About Unified Payments Interface (UPI):

- It is a system that facilitates instant fund transfer between two bank accounts on a mobile platform, without requiring details of the beneficiary’s bank account.

- It is an advanced version of Immediate Payment Service (IMPS) round–the-clock funds transfer service to make cashless payments faster, easier and smoother.

- It is developed by National Payment Corporation of India (NPCI) and regulated by RBI.

- NPCI launched UPI with 21 member banks in 2016.

- India is expanding UPI based infrastructure in many foreign countries such as Singapore’s PayNow has been linked with UPI.

Importance of UPI:

- With the mushrooming of mobile wallets, QR-based apps and the Unified Payments Interface (UPI), the volume of digital transactions leapfrogged from 293 crore in March 2020 to 799 crore by March 2022, as per RBI data.

- But CIC (currency in circulation) as a proportion of GDP has been rising too.

- After hovering at 11-12 per cent until FY20, it hit 14 per cent in FY21 and remained at 13 per cent in FY22.

- CIC in developed economies tends to be in the single digits.

- But a recent study by SBI Ecowrap offers hope that digital payments may finally be reducing the need for hard cash, in some respects.

- For the first time, the Diwali week this year saw a dip in CIC as opposed to sharp spikes witnessed in the last 20 years.

- The lower need for cash can mainly be traced to the widespread adoption of UPI.

Evolution of UPI:

- UPI has gone a long way in enabling the digitalization of India’s payments economy.

- It has added layers of convenience in the way people transact with money.

- UPI being an indigenous ‘Made in India’ product has helped India find its unique place in the globe in the digital payments arena.

- Likely to be a $180 billion market by 2026, India is among top nations in this space.

- With UPI expanding beyond the borders, it has certainly brought a lot of pride to the nation.

Significance of UPI enabled payments:

- Low-Cost Source of Funds : UPI’s use prompts bank account holders to hold larger balances in their savings accounts, providing banks with a low-cost source of funds.

- UPI manages to materially reduce the need for the public to deal in cash.

- Greater traceability of transactions: Substitution of anonymous cash payments with digital ones also allows for greater traceability of transactions for the taxman looking to widen the tax base.

- Reduce Logistic Costs: If the demand for paper currency diminishes, banks would save on the logistics costs involved in safely storing and transporting paper currency and regularly refilling their ATMs.

- Increasing tax revenue: With digitalization, the market’s black money can be diminished, increasing compliance and increasing tax revenue.

Key Issues associated with UPI payment systems:

- High transaction failure rates: Digital payments are currently characterised by high transaction failure rates.

- A Large Number of people left Behind: With options such as mobile wallets, payment apps and QR code readers available only on smartphones, feature phone users who make up roughly half of India’s mobile subscriber base have been left behind.

- Many people lack digital literacy: Since most people lack digital literacy, they are unable to use the UPI system.

Way Forward:

- There has to be widespread awareness campaign to educate users about the safe use of UPI and the convenience it brings.

- Digital payment services like UPI were currently used by just a fifth of the population.

- Unless a third adopted it, cash in circulation would not see a durable reduction.

Despite affluent consumers embracing them in a big way, digital payments are still far from ubiquitous. Policymakers may need to address all the issues to further the reach of digital payments.

Additional Information:

- Currency in circulation refers to the amount of cash–in the form of paper notes or coins–within a country that is physically used to conduct transactions between consumers and businesses.

- Currency in circulation is all of the money that has been issued by a country’s monetary authority, minus cash that has been removed from the system.

- It represents part of the overall money supply, with a portion of the overall supply being stored in checking and savings accounts.

Source: The Hindu

Previous Year Question

Q.1) Which of the following is the most likely consequence of implementing the ‘Unified Payments Interface (UPI)’?

- Mobile wallets will not be necessary for online payments.

- Digital currency will totally replace the physical currency in about two decades.

- FDI inflows will drastically increase.

- Direct transfer of subsidies to poor people will become very effective.