Environment & Ecology, Governance

Context: Efforts are being made by Governments, civil societies, corporates, businesses and even the common people towards net-zero emissions to nullify climate change and global warming. India is in the driver’s seat in these efforts and can explore a new dimension of taxing emissions which will augment the government revenues.

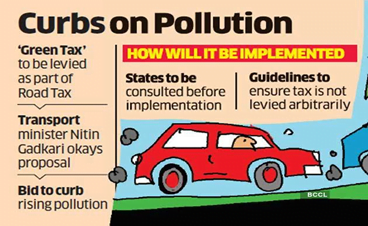

About Green Tax:

- A Green Tax is a type of tax levied by the government for the purpose of environmental conservation.

- It is believed charging taxes on emissions that cause pollution will lower environmental impairment in a cost-effective manner by encouraging behavioural changes in households and firms that need to decrease their pollution.

- The revenue collected through such tax can be used to create green energy infrastructure, combat environmental pollution, afforestation and other such purposes which help in conserving the environment.

- In India, many state governments such as Goa and Gujarat have provision for green tax or cess.

- The Ministry of Road Transport and Highways (MoRTH) had introduced a similar tax called Green Tax / Eco Tax on older vehicles.

Need for a Green tax

- The government has been looking at different ways of augmenting its revenues because tax buoyancy cannot rely upon mere growth levels which can vary and abnormal situations (e.g., COVID-19) may affect them.

(Tax buoyancy is an Economic theory concept that explains the relationship between the changes in the government’s tax revenue growth and the changes in GDP. It refers to the responsiveness of tax revenue growth to changes in GDP.)

- Usually faulty taxing policies of governments led to existing taxpayers being taxed even more in the name of environmental taxes or otherwise.

- As the country goes digital and most business units are GST-registered, we have records of activities of each firm and we can consider taxing companies that pollute the environment.

- This universe of companies can serve as the taxable base on which a green tax can be levied.

- Even a rudimentary activity like farming causes pollution and this tax can be imposed at the mandi level, the official point of sale.

Potential of revenue generation through green taxing in India:

- India’s top 4,000 odd companies had a combined turnover of roughly ₹100 trillion in 2021-22.

- Intuitively, if a small green tax is imposed on the sales of these companies linked to pollution it may fetch large revenues.

- For example an average green tax at 0.5% of the turnover will generate ₹50,000 crores annually for the government.

- This can be used to finance budget spending and it will complement the government’s efforts of issuing green bonds for projects that are environmentally compliant.

- The green tax need not be uniformly applied, and its rate could vary from 0.1% to 2%, depending on the industry concerned.

- As the sales of these companies/ industries grow, they would automatically yield higher revenues to the government.

Methods of calculating pollution emitted by individual business activity and taxing it: There are different ways of arriving at the amount of pollution emitted by every business activity.

- The current data shows that the industries/ sectors based on fossil fuels are most polluting such as manufacturing and construction, services, transport, chemicals and fertilizers etc.

- Services with no factories add to ecological atrophy with their buildings (fancy glass-front edifices of modern commercial complexes and cooling emissions) and servers that add to global warming.

- The Centre can commission research agencies to independently evaluate the emissions of all industries and set standards for the same.

- Once these standards are in place these industries can be taxed on the basis of the pollution caused by their business activity.

- Using broad industry averages emission as the norm:

- Initially the companies can be slotted into industry groups based on how their production or sales are classified.

- A cut-off level of 50% of product sales or production can be used for classification.

- The product with the largest share in a company’s overall production or sales can determine its industry assignment.

- Assessment of pollutant emissions can be reviewed periodically, as firms would be expected to do their utmost to induct new technologies and reduce their emissions over time.

- This would ensure that the businesses pay for the damage caused to the environment.

- Hence the Green Tax would be a levy based on the status of the company and defined by the industry to which it belongs.

Challenges of imposing Green Tax on all business:

- Assessing individual firm’s emissions with accuracy and proportional tax rate is a difficult process and presently there is no such robust technology in existence.

- Companies may pass the tax cost onto the customers which may lead to inflation and a rise in prices, such steps are not desirable for vulnerable sections.

- Lack of enforcement at the grassroots plagued by corruption may lead such initiatives to become just one more tax among the many.

- It may hamper the small and local industries, MSMEs as their costs will increase which will reduce their competitiveness.

- Some companies have been observed to indulge in ‘greenwashing’ just to meet CSR obligations and may find such loopholes for the Green taxing as well.

Way Forward:

A Green Tax could be a right step on the lines of single taxing for emissions but it poses many challenges such as passing of costs onto the customers but it would not be very significant and can be absorbed. Moreover, consumers of products and services that are environmentally unfriendly would also be made accountable to the world at large. All in all the cost has to be borne by somebody but the government is sure to be a big beneficiary.

Source: LiveMint

Previous Year Question

Q.1) Which one of the following best describes the term “greenwashing”? (2022)

- Conveying a false impression that a company’s products are eco-friendly and environmentally sound

- Non-inclusion of ecological/ environmental costs in the Annual Financial Statements of a country

- Ignoring the consequences disastrous ecological while infrastructure development undertaking

- Making mandatory provisions for environmental costs in a government project/programme